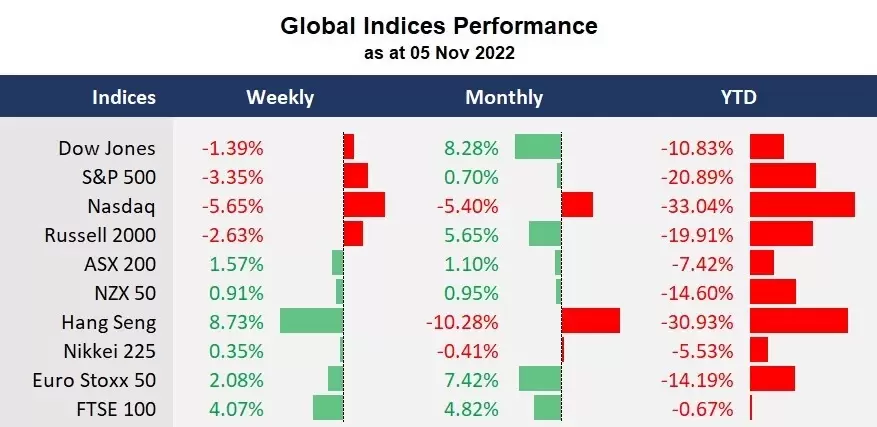

Fed Chair Jerome Powell’s reiteration of his hawkish stance dashed hopes for a Fed pivot last week, though a slowdown in rate hikes may be on the table. While all the major US indices closed lower for the week, China’s reopening optimism sent Hong Kong stock markets up 8%, reversing the prior week’s losses and pumping up global commodity prices. This week, the US midterm election and the CPI data will be in focus, where a further decline in inflation may offer a buffer to the bear markets. It is also worth noting that the US stocks have all had positive returns within 12 months after midterm in history, will this time be the same?

What are we watching?

- US bond yields stay high: The bond yields continued to rise after Fed Chair Powell indicated a higher peak in rates, with the 2-year bond yield rising to the highest seen in July 2007.

- The US dollar pulls back: The US dollar index pulled back from a week high of above 113 to 110.68 after the US job data showed a rise in the unemployment rate. However, it is too early to say the dollar has hit a peak since bond yields stay high.

- A jump in commodity prices: China’s reopening optimism boosted commodity prices on Friday, with both gold and silver reaching their 4-week highs. And crude oil prices surged more than 5% on Friday, with the WTI futures closing above 90 for the first time in one month.

- Both Yuan and Chinese shares rebound: Both the Chinese Yuan and Chinese stock markets jumped amid China’s reopening hope, with USD/CNH pulling back from a week high of above 7.3570 to 7.1773 and the Hang Seng Index rising 8% last week. However, Beijing has never officially confirmed to exit the Zero-covid policy, which makes it doubtful for the rebounding frenzy.

- Cryptocurrencies rise: Cryptocurrencies were resilient in the last few weeks and did not follow the stock markets’ volatility. Both Bitcoin and Ethereum rose to a two-month high, while Polygon soared to 1.2, the highest seen in April.

Economic Calendar (07 Nov – 11 Nov)